.jpg?width=804&height=536&name=GettyImages-1309300677%20(1).jpg)

We maintain a positive view of fixed income as it appears rates have peaked, growth trajectories are slowing (making less risky assets relatively more appealing), and yields are starting the year at an attractive level. We believe this could cause the yield curve to re-steepen and lead to less inverted, or even positive, sloping curves.

2023 overview

2023 was a volatile year for fixed income, as yields were whipsawed by the combination of rate hikes and tightening monetary policy. The failures of Silicon Valley Bank and Credit Suisse in March led to fears of a broader regional banking crisis and opened the door to debate over whether rates had peaked and if a cutting cycle would soon follow. These arguments proved to contain little credence in 2023, as the Federal Reserve continued hiking rates until the May meeting, then paused for a couple of meetings before hiking again in July.

The Bank of Canada took a slightly different approach, hiking rates once in January before pausing until June and tightening twice more before the end of the year.

hiking rates once in January before pausing until June and tightening twice more before the end of the year.

In both countries, inflation remained elevated but began to decline.

The collapse of Silicon Valley Bank and Credit Suisse also shook corporate bonds, as spreads peaked in March over fears of a broader bank failure. As these issues proved to be relatively contained and economic data and corporate earnings both came in strong, credit spreads and other risk assets rallied and priced in the potential for a soft landing for the economy.

Despite the high volatility throughout the year, credit spreads across the risk spectrum finished the year tighter.1

2024 Fixed income outlook

As we enter 2024, we believe that rates have peaked in both Canada and the U.S.,  and the focus has shifted away from further rate hikes towards when easing will take place, and by how much. Inflation has eased in much of the developed world, and we believe that it will continue to move lower throughout the year, however, remain above the 2% level targeted by central banks.

and the focus has shifted away from further rate hikes towards when easing will take place, and by how much. Inflation has eased in much of the developed world, and we believe that it will continue to move lower throughout the year, however, remain above the 2% level targeted by central banks.

Economic growth has downshifted as a result of the rate hiking campaigns. We expect to see the lagged effects of tighter policy throughout 2024 as the effects of the higher rates continue to transmit throughout the economy.

We maintain a positive view of fixed income as it appears rates have peaked, growth trajectories are slowing (making less risky assets relatively more appealing), and yields are starting the year at an attractive level. We believe this could cause the yield curve to re-steepen and lead to less inverted, or even positive, sloping curves.

Government bonds

Canada

Given the interest rate sensitivity of the Canadian economy, the impact of the rate hikes have been effective in restraining the economy, which has been slowing through the second and third quarters of 2023.2 According to the Bank of Canada, the economy is no longer reflecting excess demand, and the upward risk of inflation is balanced with the downside risk of a slowing economy. Market sentiment suggests easing may begin as early as the first quarter in 2024, but we believe that the timing is optimistic given the progress that has been made on inflation. However, the Bank of Canada has previously acknowledged that rate cuts could begin before inflation is sustainably at 2%, depending on market conditions.

Key areas we will continue to monitor include inflation, particularly core inflation and inflation expectations, and wage and job growth, which remain at elevated levels.

United States

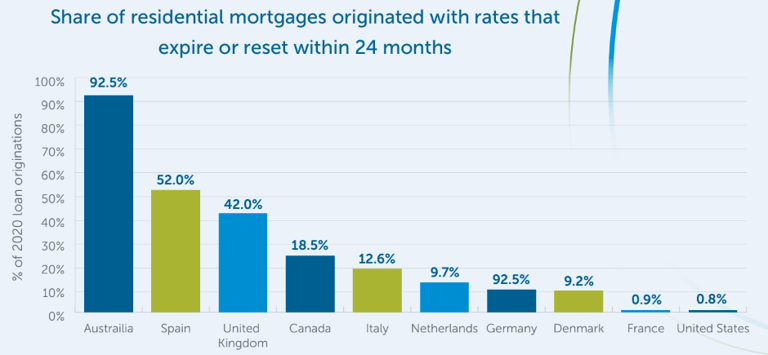

The U.S. economy has remained more resilient than the Canadian economy, given lower levels of interest rate sensitivity, which is particularly noticeable in the housing market due to longer-dated fixed mortgages south of the border, versus the shorter resets in Canada.

Source: Fitch Ratings Share of residential mortgages originated with rates that expire or reset within 24 months Expressed as % of 2020 loan originations. Analysis as of December 2022.

The American consumer has also remained more resilient as wage growth and employment have remained robust.3

We’ll continue to monitor inflation expectations which remain elevated, and employment growth which is starting to show some signs of softening. Inflation has also been trending lower in the U.S. but given a more resilient economy, the Fed may not feel the need to cut rates as early, or by as much, as markets currently expect.

Corporate bonds

We see the potential for a wide range of outcomes as the market appears to be pricing in a high probability of a soft landing as described in the macroeconomic outlook. However, we believe that this scenario remains uncertain.

Investment grade

Heading into the new year, our base case for higher quality corporate bonds is that credit spreads are likely to widen, but not significantly. Higher-quality investment grade bonds tend to be issued by businesses with more resilient business models that can withstand economic downturns and tend to be less impacted by increasing spreads if economic growth slows further. Furthermore, investment-grade companies generally find it easier to maintain access to capital markets to refinance debt maturities, making them less likely to be affected by tighter lending conditions if growth slows significantly.

High yield

Although balance sheet fundamentals remain strong, we have seen some deterioration. After six consecutive quarters between Q1 2021-Q2 2022 where credit rating upgrades have exceeded downgrades, the past six quarters (from Q3 2022 to Q4 2023) have seen the opposite occur. In addition, historically low default rates have hovered around 1% for all of 2022. In 2023, default rates have increased to roughly 2.5%4 and most market strategists expect them to increase further by up to 2% to 4.5%.

As with past default cycles, defaults will be heavily skewed towards companies with lower-quality balance sheets and ratings. We expect that there will be pressure on companies rated CCC- and below, and that overall spreads will widen. However, increasing amounts of capital raised in private credit markets could mitigate the default rate as private credit investors look to deploy capital.

![]() Download the full Empire Life 2024 Market Outlook (PDF).

Download the full Empire Life 2024 Market Outlook (PDF).

1 Bloomberg, November 30, 2023

2 Stats Canada, September 30 2023

3 OECD, 2023 https://data.oecd.org/hha/household-debt.htm

4 Bank of America Securities, December 2023

This document reflects the views of Empire Life as of the date published. The information in this document is for general information purposes only and is not to be construed as providing legal, tax, financial or professional advice. The Empire Life Insurance Company assumes no responsibility for any reliance on or misuse or omissions of the information contained in this document. Please seek professional advice before making any decisions.

Policies are issued by The Empire Life Insurance Company. A description of the key features of the individual variable insurance contract is contained in the Information Folder for the product being considered. Any amount that is allocated to a Segregated Fund is invested at the risk of the contract owner and may increase or decrease in value. Past performance is no guarantee of future performance.

Information contained in this report has been obtained from third party sources believed to be reliable, but accuracy cannot be guaranteed. Empire Life Investments Inc. is the Portfolio Manager of certain Empire Life segregated funds. Empire Life Investments Inc. is a wholly-owned subsidiary of The Empire Life Insurance Company.

March 2024